All Categories

Featured

Table of Contents

The are entire life insurance coverage and global life insurance policy. The money value is not added to the fatality advantage.

The plan lending interest price is 6%. Going this path, the rate of interest he pays goes back right into his plan's money value instead of an economic institution.

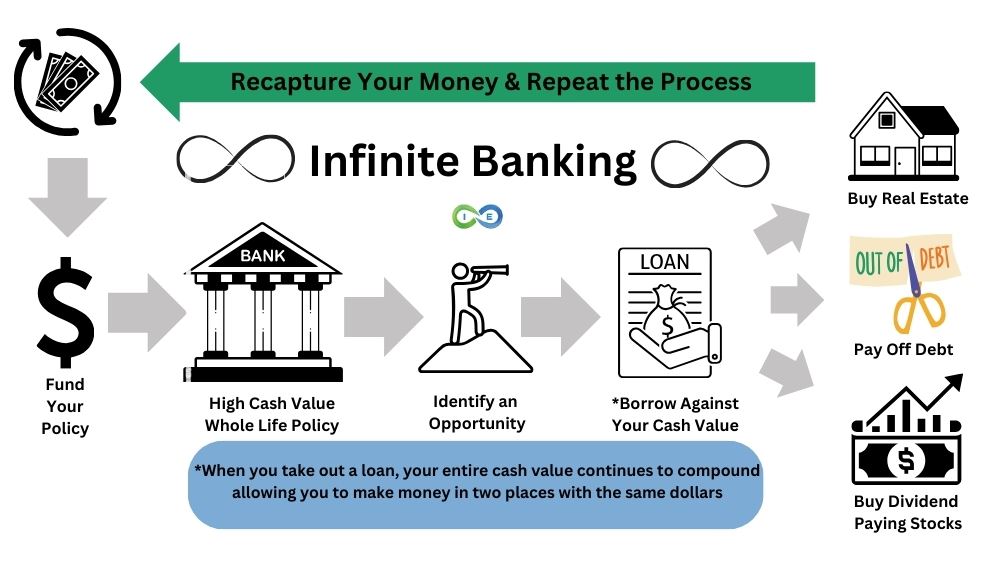

Visualize never having to stress regarding financial institution lendings or high interest prices once more. That's the power of boundless banking life insurance policy.

There's no set lending term, and you have the liberty to choose on the settlement schedule, which can be as leisurely as repaying the finance at the time of death. This adaptability encompasses the servicing of the car loans, where you can go with interest-only settlements, maintaining the finance balance flat and workable.

Holding money in an IUL fixed account being credited interest can often be much better than holding the cash money on deposit at a bank.: You've constantly fantasized of opening your very own bakery. You can borrow from your IUL policy to cover the first costs of renting an area, purchasing equipment, and hiring personnel.

Infinite Banking Policy

Personal financings can be acquired from conventional financial institutions and credit report unions. Obtaining cash on a credit card is typically really costly with annual percentage rates of rate of interest (APR) commonly getting to 20% to 30% or even more a year.

The tax obligation therapy of policy loans can differ substantially depending upon your country of home and the certain regards to your IUL policy. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, policy financings are normally tax-free, supplying a considerable advantage. In other territories, there might be tax obligation effects to take into consideration, such as potential tax obligations on the car loan.

Term life insurance policy just gives a survivor benefit, with no cash money value accumulation. This means there's no money value to borrow versus. This write-up is authored by Carlton Crabbe, Chief Executive Policeman of Resources forever, a specialist in offering indexed universal life insurance policy accounts. The details provided in this short article is for educational and informational purposes only and need to not be understood as economic or financial investment guidance.

Royal Bank Infinite Avion Travel Rewards

When you initially hear concerning the Infinite Financial Principle (IBC), your very first reaction may be: This seems too good to be true. Possibly you're doubtful and assume Infinite Banking is a scam or system - your own banking system. We intend to establish the record right! The problem with the Infinite Banking Idea is not the principle yet those persons supplying an adverse critique of Infinite Financial as a concept.

As IBC Authorized Practitioners through the Nelson Nash Institute, we thought we would certainly respond to some of the top questions individuals search for online when finding out and recognizing whatever to do with the Infinite Financial Principle. So, what is Infinite Banking? Infinite Financial was created by Nelson Nash in 2000 and fully described with the publication of his book Becoming Your Own Banker: Unlock the Infinite Financial Principle.

Infinite Banking Video

You assume you are coming out financially ahead because you pay no passion, yet you are not. With conserving and paying money, you may not pay rate of interest, however you are utilizing your money as soon as; when you spend it, it's gone forever, and you offer up on the possibility to earn life time substance rate of interest on that cash.

Also banks use entire life insurance coverage for the same functions. The Canada Revenue Firm (CRA) also recognizes the worth of participating whole life insurance coverage as a distinct property course utilized to create long-lasting equity securely and predictably and supply tax benefits outside the range of typical financial investments.

Ibc Concept

It permits you to generate riches by meeting the banking feature in your own life and the capacity to self-finance significant way of living acquisitions and expenditures without disrupting the compound interest. One of the easiest methods to assume about an IBC-type participating whole life insurance policy policy is it is equivalent to paying a home mortgage on a home.

With time, this would produce a "consistent compounding" result. You get the image! When you obtain from your taking part whole life insurance coverage plan, the cash money value proceeds to expand nonstop as if you never ever obtained from it in the initial place. This is because you are making use of the money worth and survivor benefit as collateral for a loan from the life insurance policy firm or as security from a third-party lender (recognized as collateral lending).

That's why it's crucial to work with a Licensed Life Insurance coverage Broker accredited in Infinite Financial who structures your taking part entire life insurance plan correctly so you can prevent negative tax obligation ramifications. Infinite Financial as an economic approach is except everyone. Below are a few of the pros and cons of Infinite Banking you must seriously think about in choosing whether to relocate ahead.

Our preferred insurance policy carrier, Equitable Life of Canada, a mutual life insurance policy business, focuses on taking part entire life insurance coverage policies specific to Infinite Banking. Additionally, in a shared life insurance policy business, insurance policy holders are considered business co-owners and receive a share of the divisible surplus created yearly through dividends. We have a variety of service providers to pick from, such as Canada Life, Manulife and Sun Lifedepending on the needs of our customers.

Please likewise download our 5 Top Questions to Ask A Limitless Financial Agent Prior To You Employ Them. For more details regarding Infinite Banking see: Disclaimer: The product supplied in this e-newsletter is for informational and/or educational purposes just. The details, point of views and/or sights shared in this newsletter are those of the writers and not always those of the supplier.

Banking Life Insurance

The idea of Infinite Banking was developed by Nelson Nash in the 1980s. Nash was a finance specialist and follower of the Austrian college of economics, which promotes that the value of products aren't explicitly the result of standard economic structures like supply and demand. Instead, people value cash and products differently based upon their financial standing and demands.

One of the mistakes of typical banking, according to Nash, was high-interest prices on financings. Too lots of people, himself consisted of, got right into financial problem due to reliance on banking organizations.

Infinite Financial requires you to have your economic future. For goal-oriented people, it can be the ideal financial tool ever before. Here are the benefits of Infinite Financial: Arguably the single most valuable facet of Infinite Banking is that it improves your money flow.

Dividend-paying whole life insurance policy is very low risk and provides you, the policyholder, an excellent deal of control. The control that Infinite Financial offers can best be grouped into two groups: tax benefits and asset protections.

Entire life insurance policy policies are non-correlated possessions. This is why they work so well as the economic structure of Infinite Financial. Despite what takes place in the marketplace (supply, property, or otherwise), your insurance plan maintains its well worth. As well lots of individuals are missing out on this essential volatility barrier that helps shield and expand riches, rather splitting their money into two pails: savings account and financial investments.

Market-based investments expand wide range much quicker but are exposed to market variations, making them naturally dangerous. What if there were a 3rd pail that offered safety but additionally modest, guaranteed returns? Whole life insurance policy is that 3rd container. Not just is the price of return on your entire life insurance policy plan guaranteed, your survivor benefit and premiums are likewise assured.

Whole Life Insurance Banking

This structure straightens perfectly with the concepts of the Continuous Riches Approach. Infinite Banking appeals to those seeking greater financial control. Here are its primary benefits: Liquidity and access: Policy car loans give prompt accessibility to funds without the limitations of typical small business loan. Tax effectiveness: The cash worth grows tax-deferred, and policy finances are tax-free, making it a tax-efficient tool for developing wide range.

Possession defense: In lots of states, the money worth of life insurance policy is protected from financial institutions, including an added layer of monetary security. While Infinite Banking has its benefits, it isn't a one-size-fits-all solution, and it features significant disadvantages. Here's why it might not be the most effective strategy: Infinite Financial commonly calls for elaborate policy structuring, which can puzzle insurance policy holders.

{kind=link}

Latest Posts

How To Be My Own Bank

How To Be Your Own Bank In Canada: Infinite ...

Infinite Banking Concept Pdf