All Categories

Featured

Table of Contents

The are entire life insurance and global life insurance coverage. The money worth is not included to the fatality advantage.

After one decade, the cash money worth has grown to around $150,000. He obtains a tax-free financing of $50,000 to begin a company with his bro. The plan loan rates of interest is 6%. He settles the finance over the next 5 years. Going this path, the interest he pays returns right into his plan's cash money worth rather than a banks.

Imagine never having to fret about bank loans or high interest prices once again. That's the power of unlimited banking life insurance coverage.

There's no set finance term, and you have the flexibility to determine on the settlement routine, which can be as leisurely as paying back the lending at the time of death. This flexibility extends to the maintenance of the car loans, where you can go with interest-only settlements, maintaining the car loan equilibrium flat and convenient.

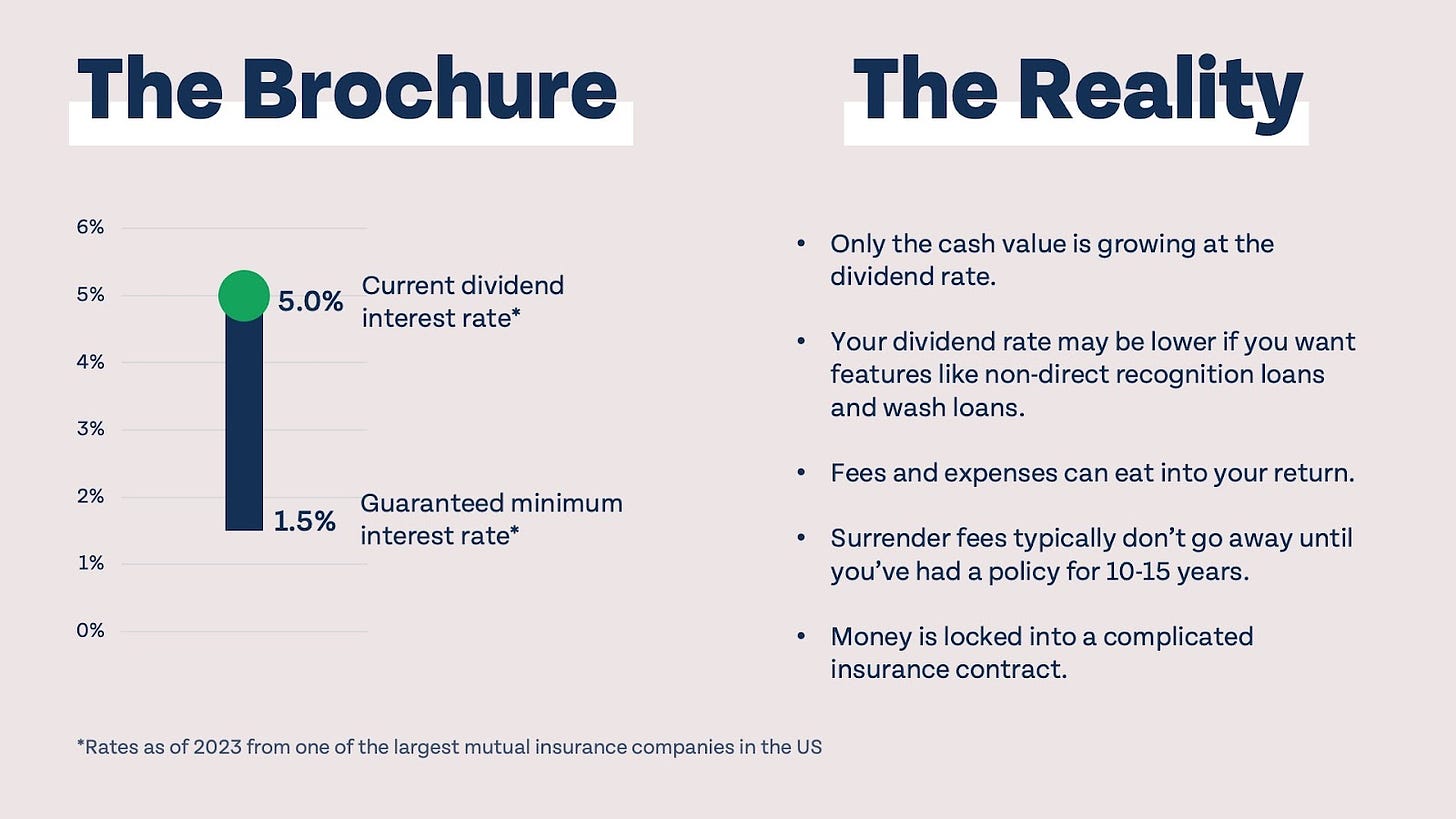

Holding money in an IUL taken care of account being credited passion can commonly be much better than holding the money on deposit at a bank.: You've always imagined opening your own bakery. You can borrow from your IUL plan to cover the preliminary expenses of leasing an area, buying equipment, and hiring personnel.

Infinite Banking Success Stories

Individual financings can be gotten from standard financial institutions and cooperative credit union. Here are some bottom lines to consider. Charge card can give a flexible method to obtain money for extremely short-term periods. Obtaining money on a debt card is usually very pricey with yearly percent rates of rate of interest (APR) typically reaching 20% to 30% or more a year.

The tax treatment of plan car loans can differ dramatically depending upon your country of house and the particular regards to your IUL plan. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan loans are generally tax-free, offering a significant advantage. In other territories, there may be tax ramifications to consider, such as prospective tax obligations on the lending.

Term life insurance coverage only offers a fatality benefit, with no cash value build-up. This means there's no money worth to obtain against. This short article is authored by Carlton Crabbe, President of Capital forever, a specialist in giving indexed universal life insurance policy accounts. The information supplied in this article is for educational and informative functions only and ought to not be interpreted as economic or investment recommendations.

Nelson Nash Net Worth

When you initially find out about the Infinite Banking Concept (IBC), your very first reaction could be: This seems too great to be real. Possibly you're cynical and assume Infinite Financial is a rip-off or system - does infinite banking work. We wish to establish the record right! The trouble with the Infinite Banking Idea is not the concept however those individuals offering an adverse review of Infinite Banking as a principle.

So as IBC Authorized Practitioners via the Nelson Nash Institute, we thought we would address some of the top questions individuals search for online when finding out and comprehending everything to do with the Infinite Financial Principle. So, what is Infinite Financial? Infinite Banking was produced by Nelson Nash in 2000 and completely explained with the publication of his book Becoming Your Own Banker: Unlock the Infinite Financial Principle.

Can You Be Your Own Bank

You think you are coming out monetarily in advance because you pay no rate of interest, but you are not. When you conserve money for something, it normally suggests sacrificing something else and cutting down on your lifestyle in other areas. You can duplicate this procedure, however you are simply "reducing your method to wide range." Are you delighted living with such a reductionist or scarcity attitude? With conserving and paying money, you might not pay interest, however you are using your money as soon as; when you invest it, it's gone forever, and you quit on the chance to earn life time compound interest on that particular money.

Even banks make use of whole life insurance coverage for the exact same objectives. The Canada Revenue Company (CRA) even acknowledges the worth of taking part whole life insurance coverage as a distinct possession class used to generate lasting equity securely and naturally and supply tax obligation advantages outside the range of conventional investments.

Life Insurance Infinite Banking

It enables you to generate wide range by satisfying the financial feature in your very own life and the ability to self-finance major way of living purchases and expenditures without interrupting the substance rate of interest. One of the most convenient methods to think of an IBC-type participating entire life insurance policy policy is it is comparable to paying a home mortgage on a home.

Over time, this would develop a "consistent compounding" result. You understand! When you obtain from your taking part whole life insurance coverage plan, the cash money value continues to grow nonstop as if you never ever obtained from it in the first place. This is since you are utilizing the cash worth and death benefit as security for a car loan from the life insurance policy firm or as collateral from a third-party lender (referred to as collateral loaning).

That's why it's critical to deal with a Licensed Life insurance policy Broker accredited in Infinite Banking who frameworks your taking part entire life insurance policy policy properly so you can avoid unfavorable tax implications. Infinite Banking as a financial approach is not for everybody. Here are a few of the benefits and drawbacks of Infinite Financial you need to seriously think about in determining whether to progress.

Our preferred insurance policy service provider, Equitable Life of Canada, a common life insurance policy business, concentrates on taking part entire life insurance policy plans particular to Infinite Banking. Likewise, in a common life insurance coverage company, insurance policy holders are taken into consideration firm co-owners and get a share of the divisible excess created each year with returns. We have a range of providers to choose from, such as Canada Life, Manulife and Sun Lifedepending on the requirements of our customers.

Please also download our 5 Leading Questions to Ask An Unlimited Banking Agent Prior To You Hire Them. For more details concerning Infinite Banking check out: Disclaimer: The material supplied in this newsletter is for informational and/or academic purposes only. The details, viewpoints and/or views revealed in this newsletter are those of the writers and not necessarily those of the representative.

The Banking Concept

Nash was a finance professional and follower of the Austrian college of business economics, which advocates that the value of products aren't explicitly the outcome of standard economic frameworks like supply and demand. Instead, people value cash and products differently based on their economic status and needs.

One of the challenges of typical financial, according to Nash, was high-interest rates on lendings. Way too many individuals, himself included, entered economic difficulty because of reliance on financial establishments. As long as financial institutions established the rates of interest and car loan terms, individuals didn't have control over their own wide range. Becoming your very own lender, Nash identified, would place you in control over your monetary future.

Infinite Financial requires you to possess your financial future. For goal-oriented individuals, it can be the ideal economic device ever before. Here are the advantages of Infinite Banking: Perhaps the single most valuable aspect of Infinite Banking is that it enhances your cash circulation.

Dividend-paying entire life insurance policy is really low risk and offers you, the insurance holder, a great deal of control. The control that Infinite Financial provides can best be grouped into 2 classifications: tax obligation benefits and property securities.

Entire life insurance policies are non-correlated possessions. This is why they work so well as the economic structure of Infinite Banking. No matter of what occurs in the market (supply, real estate, or otherwise), your insurance policy preserves its worth.

Market-based financial investments expand wide range much quicker yet are subjected to market variations, making them inherently risky. What happens if there were a 3rd bucket that offered safety however additionally moderate, guaranteed returns? Entire life insurance policy is that third pail. Not just is the price of return on your whole life insurance policy ensured, your death benefit and premiums are also guaranteed.

Be My Own Banker

This structure straightens perfectly with the principles of the Perpetual Wide Range Strategy. Infinite Banking attract those seeking higher financial control. Below are its primary advantages: Liquidity and accessibility: Plan finances supply immediate access to funds without the restrictions of traditional small business loan. Tax obligation effectiveness: The cash money worth grows tax-deferred, and plan lendings are tax-free, making it a tax-efficient tool for constructing wealth.

Asset protection: In several states, the money worth of life insurance is secured from financial institutions, adding an extra layer of monetary safety and security. While Infinite Financial has its qualities, it isn't a one-size-fits-all option, and it features substantial disadvantages. Below's why it might not be the most effective technique: Infinite Banking usually requires elaborate policy structuring, which can perplex insurance policy holders.

{kind=link}

Latest Posts

How To Be My Own Bank

How To Be Your Own Bank In Canada: Infinite ...

Infinite Banking Concept Pdf